HSA Max Contributions 2025: Optimize Health Savings

Understanding the 2025 HSA max contributions is crucial for optimizing your health savings and achieving significant financial benefits, including triple tax advantages and investment growth.

Are you ready to unlock a powerful financial tool for your health and future wealth? Delving into the details of

HSA max contributions for 2025: Leveraging Health Savings for Financial Gain is not just about understanding numbers; it’s about strategizing for a more secure tomorrow. This guide will illuminate how maximizing your Health Savings Account can be a cornerstone of your financial planning, offering benefits far beyond mere healthcare coverage. Join us as we explore the nuances and advantages of this often-underestimated financial vehicle.

Understanding HSA Basics and Eligibility for 2025

Before diving into the specifics of 2025 contribution limits, it’s essential to grasp the fundamental nature of a Health Savings Account (HSA) and who qualifies for one. An HSA is a tax-advantaged savings account that can be used for qualified medical expenses. Unlike a Flexible Spending Account (FSA), HSA funds roll over year after year, accrue interest, and can even be invested, making them a unique blend of healthcare savings and long-term investment opportunity.

Eligibility for an HSA is tied directly to enrollment in a High-Deductible Health Plan (HDHP). For 2025, specific criteria will define what constitutes an HDHP, primarily focusing on minimum deductible amounts and maximum out-of-pocket limits. These thresholds are set annually by the IRS and are critical for determining if your health insurance plan allows you to contribute to an HSA.

Key HSA Eligibility Criteria

- Must be covered under a High-Deductible Health Plan (HDHP).

- Must not be covered by any other health insurance that is not an HDHP (with some exceptions for specific limited-purpose coverage).

- Must not be enrolled in Medicare.

- Must not be claimed as a dependent on someone else’s tax return.

Meeting these criteria is the first step toward leveraging the powerful benefits an HSA offers. It’s not just about having an HDHP; it’s about ensuring your overall health coverage situation aligns with IRS regulations to avoid penalties and maximize the account’s potential. Understanding these foundational rules ensures you can confidently plan your contributions for the upcoming year.

The IRS typically releases the new contribution limits and HDHP definitions well in advance, providing ample time for individuals and employers to adjust their financial strategies. Staying informed about these annual adjustments is paramount for anyone looking to optimize their health savings. For 2025, these figures will reflect adjustments for inflation and healthcare cost trends, making it vital to consult the latest official guidance.

The Anticipated HSA Max Contributions for 2025

The core of financial planning with an HSA revolves around understanding the maximum amounts you can contribute each year. While the official numbers for 2025 are typically announced by the IRS in the latter half of the preceding year, projections can often be made based on inflation trends and historical adjustments. These limits are crucial because contributing the maximum allowed can significantly amplify your tax benefits and long-term savings potential.

For individuals, the self-only coverage limit is one figure, and for families, the family coverage limit is another, usually substantially higher. These limits represent the total amount that can be contributed by both the employee and the employer combined in a calendar year. Additionally, individuals aged 55 and older are often eligible for an extra catch-up contribution, further boosting their savings capacity as they approach retirement.

Projected 2025 Contribution Limits (Illustrative)

Based on recent inflationary adjustments and historical patterns, we can anticipate the 2025 figures to slightly increase from 2024. For instance, if 2024 saw self-only contributions at $4,150 and family contributions at $8,300, a modest increase of 2-3% might push these figures to approximately $4,250 for self-only and $8,500 for family coverage in 2025. The catch-up contribution for those 55 and over is usually a fixed additional amount, such as $1,000, which tends to remain stable for several years.

- Self-Only Coverage: Expected to be around $4,250 – $4,300

- Family Coverage: Expected to be around $8,500 – $8,600

- Catch-Up Contribution (Age 55+): Expected to remain at $1,000

These projected figures are estimates and should not be taken as definitive until official IRS announcements. However, they provide a valuable benchmark for individuals and families to begin planning their contributions. Maximizing these limits is key to fully harnessing the triple tax advantage that HSAs offer, making your healthcare dollars work harder for you today and in the future.

Staying updated on the official IRS announcements is vital. Once the 2025 limits are confirmed, individuals should review their contribution strategies to ensure they are on track to meet or exceed their savings goals. This proactive approach ensures you’re always making the most of your HSA.

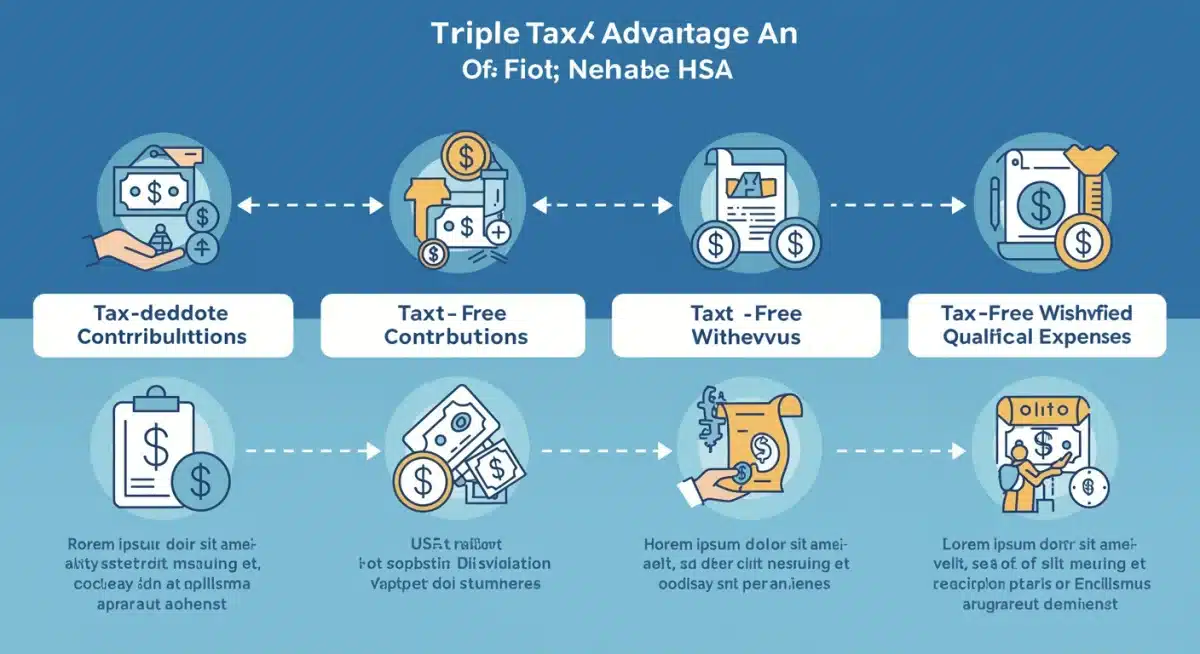

The Triple Tax Advantage: Why Maximize Your HSA?

The allure of an HSA lies in its unparalleled triple tax advantage, a benefit that sets it apart from almost any other savings vehicle. Understanding these three pillars of tax efficiency is crucial for anyone considering to maximize their

HSA max contributions for 2025 and beyond. This unique structure allows your money to grow and be used for healthcare expenses in the most tax-efficient way possible, providing significant financial relief and long-term wealth building.

Firstly, contributions to an HSA are tax-deductible. Whether you contribute through payroll deductions or directly to your account, these amounts reduce your taxable income. This immediate tax break can significantly lower your annual tax liability, effectively giving you a discount on every dollar you save for healthcare. It’s like getting a bonus just for being financially responsible with your health.

Secondly, the funds within your HSA grow tax-free. This includes any interest earned, dividends from investments, or capital gains. Unlike a standard brokerage account where investment earnings are taxed annually, your HSA investments compound without being eroded by taxes. Over decades, this tax-free growth can lead to a substantial sum, far exceeding what would be possible in a taxable account, especially when you consistently hit the

HSA max contributions for 2025. This growth potential is where the HSA truly shines as a retirement savings vehicle.

Unlocking the Power of Tax-Free Growth

- Compounding Interest: Your savings grow exponentially over time without tax drag.

- Investment Opportunities: Many HSA providers allow you to invest funds in mutual funds, ETFs, and other assets, mirroring a traditional retirement account.

- Long-Term Wealth Building: The tax-free growth makes HSAs an excellent complement to 401(k)s and IRAs for retirement planning.

Finally, withdrawals from an HSA for qualified medical expenses are tax-free. This means that when you use your HSA funds to pay for deductibles, co-pays, prescriptions, or a wide range of other eligible healthcare costs, you won’t pay a penny in taxes on those withdrawals. This third tax advantage completes the cycle, making the HSA an incredibly powerful tool for managing both current and future healthcare costs without incurring tax liabilities.

This combination of tax-deductible contributions, tax-free growth, and tax-free withdrawals for medical expenses creates a financial powerhouse. For those who can afford to pay for current medical expenses out-of-pocket and allow their HSA funds to grow, the account can effectively become a supplementary retirement fund for healthcare costs in later life, making the maximization of

HSA max contributions for 2025 a highly strategic move.

Strategies for Maximizing Your 2025 HSA Contributions

Maximizing your

HSA max contributions for 2025 requires a proactive and informed approach. It’s not just about knowing the limits, but also about implementing strategies that ensure you hit those targets consistently throughout the year. For many, this means setting up automatic contributions and regularly reviewing their financial situation to ensure they are on track to leverage the full potential of their HSA.

One of the most effective strategies is to set up payroll deductions for your HSA contributions. This method offers a “set it and forget it” convenience, ensuring that a portion of each paycheck automatically goes into your account. Many employers also contribute to HSAs, and these contributions count towards the annual maximum. Understanding your employer’s contribution schedule is vital to avoid over-contributing, though most payroll systems are designed to prevent this.

Effective Contribution Methods

- Payroll Deductions: Automate contributions directly from your paycheck, often saving on FICA taxes.

- Lump Sum Payments: If you receive a bonus or a tax refund, consider contributing a lump sum to quickly reach your annual limit.

- Regular Bank Transfers: Set up recurring transfers from your checking or savings account to your HSA if payroll deductions aren’t an option or if you need to make up a shortfall.

Another key strategy involves being mindful of the catch-up contribution if you are aged 55 or older. This additional $1,000 contribution can significantly boost your HSA balance, especially as you approach retirement when healthcare costs tend to rise. Both spouses can make a catch-up contribution if both are 55 or older and have their own HSA accounts, even if one spouse is covered under the other’s family HDHP.

Furthermore, consider the tax-deductible nature of direct contributions. If you make contributions outside of payroll deductions, remember to claim these on your tax return. This can be particularly useful if you find yourself with extra funds late in the year and want to top off your HSA before the tax deadline. The deadline for contributing to an HSA for a given tax year is typically the tax filing deadline for that year, usually April 15th of the following year.

Regularly reviewing your budget and financial goals will help you identify opportunities to increase your contributions. Even small, consistent increases can make a big difference over time, especially when combined with the tax-free growth of your investments. By being diligent and strategic, you can ensure you fully utilize the

HSA max contributions for 2025 and build a robust healthcare savings safety net.

Investing Your HSA Funds for Long-Term Growth

One of the most powerful, yet often underutilized, aspects of Health Savings Accounts is the ability to invest the funds for long-term growth. Unlike typical savings accounts that offer minimal interest, many HSA providers allow beneficiaries to invest their balances in a variety of options, similar to a 401(k) or IRA. This investment capability is a game-changer for those looking to truly leverage

HSA max contributions for 2025 into a significant financial asset for future healthcare needs, or even retirement.

The key to successful HSA investing is to treat it as a long-term retirement account. If you can afford to pay for current medical expenses out-of-pocket, allowing your HSA funds to grow untouched through investments can yield substantial returns over decades. This strategy maximizes the triple tax advantage, as both your contributions and your investment earnings grow tax-free, and qualified withdrawals remain tax-free.

Smart Investment Approaches for HSAs

- Diversification: Just like any investment portfolio, diversify your HSA investments across different asset classes, such as stocks, bonds, and mutual funds, to mitigate risk.

- Long-Term Horizon: Since healthcare costs are a lifelong concern, adopt a long-term investment horizon, allowing your investments ample time to grow and ride out market fluctuations.

- Low-Cost Index Funds/ETFs: Consider investing in low-cost index funds or Exchange Traded Funds (ETFs) to minimize fees and maximize returns, a common strategy for long-term growth.

- Risk Tolerance: Align your investment choices with your personal risk tolerance. Younger individuals might opt for more aggressive growth strategies, while those closer to retirement might prefer more conservative options.

Many HSA administrators offer a range of investment options, from conservative money market accounts to more aggressive stock and bond funds. Researching these options and understanding the associated fees is crucial. Some HSAs require a minimum cash balance before you can invest, so be aware of any such thresholds.

The power of compounding interest, combined with the tax-free growth, means that even modest returns can lead to a significant sum over 20 or 30 years. Imagine having a six-figure account exclusively for healthcare costs in retirement – that’s the potential of maximizing your

HSA max contributions for 2025 and investing them wisely. This approach moves the HSA beyond a mere spending account to a robust wealth-building tool.

Regularly review your investment performance and adjust your portfolio as needed, especially as your financial situation and proximity to retirement change. This proactive management will ensure your HSA remains aligned with your long-term financial objectives, providing a powerful resource for future healthcare expenses.

HSA vs. Other Retirement Accounts: A Strategic Comparison

While often viewed primarily as a healthcare savings tool, the HSA’s unique tax advantages position it as a formidable component of a comprehensive retirement strategy. Comparing it with other popular retirement vehicles like 401(k)s and IRAs reveals its distinct benefits and why maximizing

HSA max contributions for 2025 can be a highly strategic financial move, even for those already saving diligently for retirement.

Traditional 401(k)s and IRAs offer tax-deductible contributions and tax-deferred growth, meaning you pay taxes upon withdrawal in retirement. Roth 401(k)s and Roth IRAs, on the other hand, feature after-tax contributions but offer tax-free withdrawals in retirement. The HSA stands out with its “triple tax advantage”: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

HSA’s Unique Position in Retirement Planning

- Healthcare Costs in Retirement: Healthcare is one of the largest and most unpredictable expenses in retirement. An HSA provides a dedicated, tax-free fund for these costs.

- Flexibility Post-65: After age 65, HSA funds can be withdrawn for any purpose without penalty, though non-medical withdrawals will be subject to ordinary income tax, similar to a traditional IRA. This flexibility makes it a powerful backup retirement fund.

- No Required Minimum Distributions (RMDs): Unlike traditional IRAs and 401(k)s, HSAs are not subject to RMDs, allowing your money to continue growing tax-free for as long as you live.

For many, the optimal strategy involves contributing enough to their 401(k) to get the full employer match, then prioritizing maximizing their HSA, and finally, contributing further to their 401(k) or an IRA. This tiered approach ensures you capture all available employer-sponsored funds while leveraging the unparalleled tax benefits of the HSA for both current and future medical expenses and potential retirement needs.

The ability to invest HSA funds, combined with the tax-free growth and withdrawals, makes it essentially a “super Roth IRA” for healthcare expenses. If you don’t use all your HSA funds for medical costs during your working years, they become a versatile retirement asset. This is why understanding and utilizing the

HSA max contributions for 2025 is not just about health, but about robust, long-term financial security.

Considering the rising cost of healthcare, having a substantial, tax-free fund specifically earmarked for these expenses can provide immense peace of mind in retirement. The HSA is truly a hybrid account that uniquely bridges the gap between healthcare savings and general retirement planning, offering benefits that are hard to match.

Common Pitfalls and How to Avoid Them with Your HSA

While the benefits of an HSA are numerous, there are common pitfalls that individuals should be aware of to ensure they fully maximize their

HSA max contributions for 2025 and avoid unnecessary complications. Understanding these potential traps can help you navigate the system effectively and ensure your HSA remains a powerful financial asset rather than a source of stress.

One of the most frequent mistakes is over-contributing to your HSA. Exceeding the annual maximum contribution limit can lead to a 6% excise tax on the excess amount for each year it remains in the account. This can significantly erode the tax advantages you’re trying to gain. It’s crucial to track all contributions, including those from your employer, to stay within the IRS-mandated limits.

Avoiding HSA Missteps

- Tracking Contributions: Keep meticulous records of all contributions from yourself and your employer to avoid exceeding the annual limit.

- Understanding HDHP Rules: Ensure your health plan continues to meet the IRS definition of an HDHP; changes in your plan could impact eligibility.

- Qualified Medical Expenses: Only withdraw funds for qualified medical expenses to maintain tax-free status. Keep receipts for all such expenses.

Another pitfall is using HSA funds for non-qualified expenses before age 65. Withdrawals for non-medical reasons prior to age 65 are subject to both ordinary income tax and a 20% penalty. This penalty can quickly negate any tax benefits you’ve accumulated. After age 65, non-qualified withdrawals are only subject to ordinary income tax, similar to a traditional IRA, offering greater flexibility.

Failing to invest HSA funds is also a missed opportunity. Many individuals treat their HSA like a standard checking account, letting funds sit in a low-interest cash option. This negates the significant long-term growth potential that comes from tax-free investing. While it’s wise to keep a small emergency fund in cash within your HSA, the majority of funds intended for long-term use should be invested strategically.

Finally, neglecting to keep proper records of medical expenses can cause issues. While you don’t need to submit receipts when you withdraw funds, the IRS can request proof that withdrawals were for qualified medical expenses during an audit. Maintaining detailed records ensures you can justify tax-free withdrawals if ever questioned. By being diligent and informed, you can steer clear of these common pitfalls and fully harness the power of

HSA max contributions for 2025.

| Key Point | Brief Description |

|---|---|

| Eligibility | Must be covered by an HDHP and not enrolled in Medicare or claimed as a dependent. |

| 2025 Contributions | Anticipated increases for self-only and family coverage, plus a $1,000 catch-up for age 55+. |

| Triple Tax Advantage | Contributions are tax-deductible, growth is tax-free, and qualified withdrawals are tax-free. |

| Investment Potential | Invest HSA funds for long-term, tax-free growth, acting as a powerful retirement asset. |

Frequently Asked Questions About HSA Max Contributions for 2025

While official figures are pending IRS release, projections suggest self-only contributions could be around $4,250-$4,300 and family contributions around $8,500-$8,600. The catch-up contribution for those 55 and older is expected to remain $1,000. These are estimates based on inflation and historical trends.

To be eligible, you must be covered under a High-Deductible Health Plan (HDHP), not be covered by other non-HDHP insurance, not be enrolled in Medicare, and not be claimed as a dependent on someone else’s tax return. Your HDHP must meet specific deductible and out-of-pocket limits set by the IRS.

Maximizing your HSA offers a triple tax advantage: contributions are tax-deductible, funds grow tax-free through investments, and withdrawals for qualified medical expenses are tax-free. This makes it an incredibly efficient savings vehicle for both healthcare and retirement planning.

Yes, many HSA providers allow you to invest funds in various options like mutual funds and ETFs, similar to a 401(k) or IRA. Investing your HSA funds can lead to significant long-term, tax-free growth, transforming your account into a powerful financial asset for future healthcare needs or retirement.

Over-contributing to your HSA can result in a 6% excise tax on the excess amount for each year it remains in the account. It’s crucial to track all contributions, including employer contributions, to ensure you stay within the IRS-mandated limits and avoid penalties.

Conclusion

Mastering

HSA max contributions for 2025: Leveraging Health Savings for Financial Gain is more than just a smart financial move; it’s a strategic pathway to enhancing your overall financial well-being. By understanding the eligibility requirements, actively pursuing the maximum allowable contributions, and wisely investing your funds, you unlock a powerful tool that offers unparalleled tax advantages. The HSA serves not only as a critical resource for managing current and future healthcare costs but also as a robust, tax-efficient component of your long-term retirement planning. Embracing these strategies today can lead to significant financial security and peace of mind for years to come.

expansion: understanding the benefits")