Federal Student Loan Forgiveness Updates April 2026: 10% Debt Relief

Federal Student Loan Forgiveness Program Updates for April 2026 introduce new 10% debt relief options, offering significant financial alleviation to eligible borrowers navigating their educational debts.

As April 2026 approaches, millions of Americans are keenly watching for the latest Federal Student Loan Forgiveness Program Updates for April 2026: Are You Eligible for the New 10% Debt Relief? This critical update could significantly reshape the financial landscape for countless individuals burdened by educational debt. Understanding the nuances of these changes is paramount for anyone seeking to alleviate their student loan obligations.

Understanding the Evolving Landscape of Student Loan Forgiveness

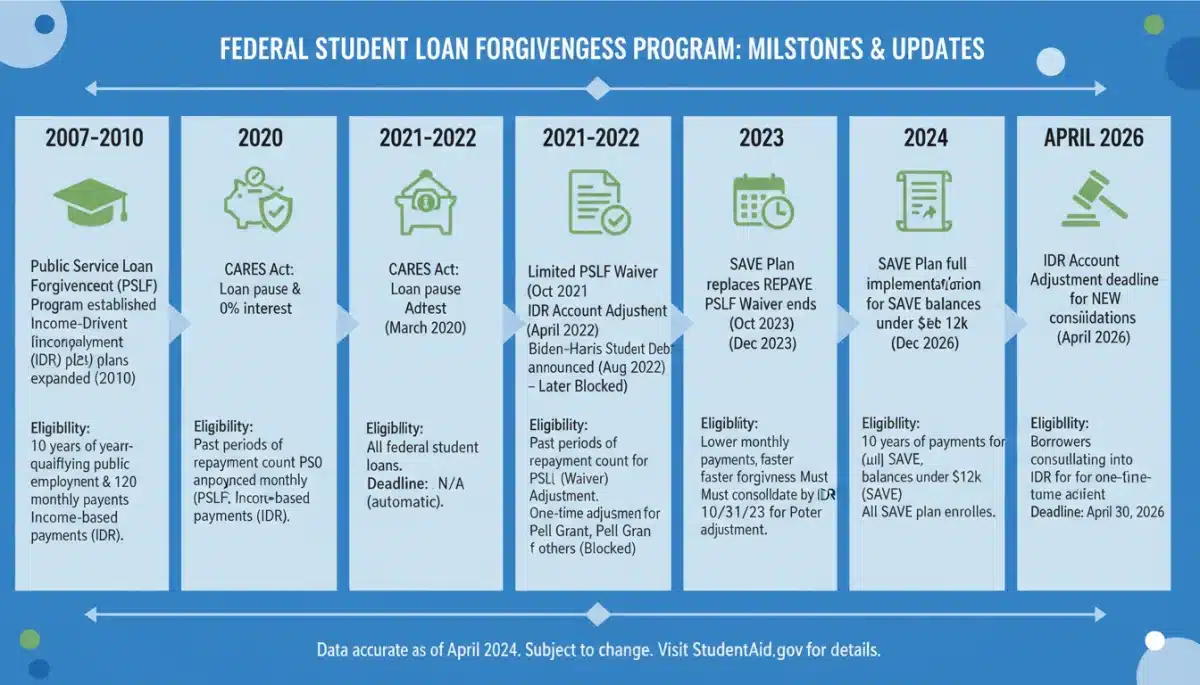

The realm of federal student loan forgiveness has been in a constant state of evolution, reflecting ongoing efforts by the government to address the escalating student debt crisis. These programs are not static; they are regularly reviewed, revised, and expanded to meet the changing economic realities and borrower needs. The updates slated for April 2026 represent another significant chapter in this ongoing narrative, bringing both new opportunities and specific requirements that borrowers must navigate carefully.

Historically, various programs have offered relief, ranging from income-driven repayment (IDR) plans that can lead to forgiveness after a certain period, to targeted programs for public service workers. However, the sheer scale of student debt has necessitated more comprehensive and accessible solutions. The federal government acknowledges the profound impact student loans have on individual financial stability and the broader economy, driving the continuous re-evaluation of existing policies and the introduction of new initiatives.

Key Shifts in Federal Policy

Recent years have seen a noticeable shift towards making forgiveness programs more inclusive and easier to access. This includes streamlining application processes and recalibrating eligibility criteria to encompass a wider array of borrowers. The April 2026 updates are expected to build upon these foundational changes, aiming to provide more immediate and tangible relief.

- Increased Accessibility: Efforts have been made to simplify the application process for various forgiveness programs, reducing bureaucratic hurdles.

- Broader Eligibility: Criteria are often revised to include more types of borrowers, such as those with older loans or specific economic hardships.

- Enhanced Communication: Government agencies are improving communication channels to ensure borrowers are aware of their options and any upcoming changes.

The continued focus on student loan forgiveness underscores a national commitment to fostering economic mobility and reducing the barriers to higher education. These programs are designed not just to alleviate individual debt but also to stimulate economic growth by freeing up borrower capital for other investments, such as homeownership or starting businesses. Therefore, staying informed about these developments is not just a matter of personal finance but also one of national economic interest.

The New 10% Debt Relief: What It Means for Borrowers

The much-anticipated new 10% debt relief initiative, effective April 2026, marks a significant development in federal student loan forgiveness. This program aims to provide a direct and immediate reduction of up to 10% on qualifying federal student loan balances for eligible borrowers. It’s designed to offer a tangible financial boost, helping borrowers reduce their principal balance and potentially lower their monthly payments over time.

This relief is distinct from previous programs, which often focused on forgiveness after extended periods of payments or service. The 10% relief is a more upfront benefit, intended to quickly alleviate a portion of the financial burden. It’s crucial for borrowers to understand that this isn’t a universal handout; specific criteria must be met to qualify. The government’s goal is to target relief where it can have the most impact, without creating undue strain on federal budgets.

How the 10% Relief Differs

Unlike some broad-based forgiveness initiatives that were temporary or faced legal challenges, this 10% debt relief is expected to be integrated into the existing framework of federal student aid, making it a more stable and predictable benefit. It complements, rather than replaces, other ongoing programs like Public Service Loan Forgiveness (PSLF) or Income-Driven Repayment (IDR) plans.

- Direct Principal Reduction: The relief directly reduces the outstanding principal balance, not just accrued interest.

- Broader Application: While specific, the eligibility criteria are designed to encompass a significant portion of federal loan borrowers.

- Immediate Impact: Borrowers who qualify could see their loan balance reduced relatively quickly after approval.

The introduction of this 10% relief also signals a potential shift in policy, moving towards more direct and calculated debt reduction strategies. This approach could serve as a model for future relief efforts, offering a middle ground between extensive forgiveness and traditional repayment plans. For borrowers, this means a renewed opportunity to reassess their repayment strategies and potentially accelerate their path to becoming debt-free.

Eligibility Criteria for the April 2026 Debt Relief

Determining eligibility for the new 10% debt relief program effective April 2026 is the first crucial step for any borrower seeking to benefit. The criteria are designed to be clear yet specific, ensuring that the relief is directed to those who meet the program’s objectives. It’s imperative for borrowers to meticulously review these requirements to avoid disappointment or delays in receiving benefits.

Generally, the program targets federal student loan borrowers, but not all federal loans may qualify. For instance, commercially held FFEL Program loans or Perkins Loans might have different pathways to eligibility or require consolidation into a Direct Consolidation Loan first. The emphasis is on Direct Loans, which are directly funded by the U.S. Department of Education.

Key Eligibility Factors

Several factors will play a role in determining who qualifies for the 10% debt relief. These typically include the type of loan, the borrower’s income level, their repayment history, and potentially their enrollment status during specific periods. The government aims to balance broad accessibility with fiscal responsibility, meaning not everyone will automatically qualify.

- Loan Type: Primarily targets Direct Loans. Borrowers with other federal loan types may need to consolidate.

- Income Requirements: There will likely be an income threshold to ensure relief is directed to those with genuine financial need.

- Repayment Status: Borrowers in good standing or those who have made consistent payments under certain plans might receive preferential consideration.

It is advisable for all federal student loan borrowers to proactively check their loan types and current repayment status. Official communications from the Department of Education or their loan servicers will provide the most accurate and up-to-date information regarding specific eligibility. Missing out on this opportunity simply due to a lack of awareness would be a significant oversight for many.

Application Process and Required Documentation for 2026

Once you’ve confirmed your potential eligibility for the new 10% debt relief, understanding the application process and gathering the necessary documentation becomes paramount. The Department of Education aims to streamline this process, but it will still require careful attention to detail to ensure a successful application. Proactive preparation can save significant time and prevent common pitfalls that might delay your relief.

The application is expected to be primarily online, accessible through the official Federal Student Aid (FSA) website. Borrowers should be wary of third-party services that promise expedited relief for a fee, as these are often scams. All legitimate federal student loan forgiveness applications are free.

Essential Steps for Application

The application process will likely involve several key steps, starting with verifying personal and loan information, followed by submitting any required supporting documents. A clear understanding of what is needed will prevent delays.

- Access the Official Portal: The application will be available on the Federal Student Aid (FSA) website. Ensure you have your FSA ID readily available.

- Verify Loan Information: Confirm all your federal loan details are accurate and up-to-date within the FSA system.

- Income Verification: You will likely need to provide recent tax returns or other income documentation to prove you meet any income thresholds.

- Submit Application: Carefully review all entered information before submitting the application electronically.

Keep copies of all submitted documents and confirmation numbers for your records. The Department of Education will likely provide a clear timeline for application review and notification of relief. Staying organized and checking the official FSA website regularly for updates will be crucial for navigating this process effectively.

Impact on Existing Loan Forgiveness Programs and Repayment Plans

The introduction of the new 10% debt relief program in April 2026 raises important questions about its interaction with existing loan forgiveness programs and repayment plans. Borrowers currently enrolled in or considering programs like Public Service Loan Forgiveness (PSLF), Income-Driven Repayment (IDR), or Teacher Loan Forgiveness need to understand how this new relief might affect their current status and future benefits. The government’s intent is typically for new programs to complement, rather than detract from, existing pathways to relief.

For many, the 10% relief could serve as an immediate reduction that lessens the overall amount to be forgiven under other programs, potentially shortening the time to full forgiveness or reducing the total interest paid. However, the specifics of how the 10% reduction is applied and accounted for within the calculations of other programs will be critical.

Synergy with Current Programs

It is anticipated that the 10% debt relief will work in conjunction with, rather than replace, existing programs. For instance, a borrower pursuing PSLF might see their qualifying balance reduced by 10%, meaning less debt to be forgiven after their 120 qualifying payments. Similarly, for IDR plans, a lower principal balance could lead to lower monthly payments, depending on the plan’s specific formula.

- PSLF: The 10% reduction could decrease the total amount forgiven after 10 years of qualifying public service.

- IDR Plans: A lower principal balance might result in reduced monthly payments and potentially accelerate the path to forgiveness if the plan is based on remaining balance.

- Teacher Loan Forgiveness: Similar to PSLF, the reduced principal could mean a smaller balance to be forgiven after meeting teaching service requirements.

Borrowers should consult with their loan servicers or the FSA website to understand the precise impact of the 10% relief on their specific circumstances and existing repayment strategies. It is vital to ensure that applying for the new relief does not inadvertently jeopardize eligibility or progress towards other forgiveness programs. A comprehensive review of all options will allow borrowers to make informed decisions that maximize their overall debt relief.

Maximizing Your Benefits: Tips for Federal Student Loan Borrowers

Navigating the complex world of federal student loan forgiveness requires a proactive and informed approach. With the Federal Student Loan Forgiveness Program Updates for April 2026, including the new 10% debt relief, there are more opportunities than ever to reduce your student debt. Maximizing these benefits means staying organized, understanding your options, and acting decisively when programs become available.

The key to success lies in continuous engagement with official sources and a clear understanding of your personal financial situation. Relying on accurate information from the Department of Education and your loan servicer is crucial to avoid misinformation and scams.

Strategic Steps for Borrowers

To ensure you take full advantage of all available relief, consider these strategic tips. These steps are designed to help you prepare for, apply to, and manage any forgiveness or relief programs effectively.

- Stay Informed: Regularly check the official Federal Student Aid (FSA) website and sign up for email updates from the Department of Education.

- Review Your Loan Portfolio: Understand your loan types (Direct, FFEL, Perkins) and current repayment status. Consolidate if necessary to qualify for more programs.

- Update Contact Information: Ensure your loan servicer and FSA have your most current mailing address, email, and phone number.

- Assess Your Eligibility: Carefully review the criteria for the 10% debt relief and any other programs you might qualify for, such as PSLF or IDR.

- Gather Documentation: Prepare necessary documents like tax returns, income statements, and employment verification well in advance of application periods.

- Beware of Scams: Never pay for help with federal loan forgiveness. All legitimate applications are free through the Department of Education.

- Consult a Counselor: If you’re unsure, consider speaking with a certified financial aid counselor for personalized advice.

By taking these steps, borrowers can position themselves to effectively leverage the April 2026 updates and other ongoing federal programs. The goal is not just to reduce debt, but to achieve greater financial stability and peace of mind, allowing you to focus on your future without the overwhelming burden of student loans.

| Key Point | Brief Description |

|---|---|

| April 2026 Debt Relief | New program offering up to 10% reduction on qualifying federal student loan balances. |

| Eligibility Criteria | Typically involves loan type (Direct Loans preferred), income thresholds, and repayment status. |

| Application Process | Online application via Federal Student Aid (FSA) website, requiring personal and income documentation. |

| Impact on Existing Programs | Complements PSLF and IDR, potentially reducing total amount to be forgiven or monthly payments. |

Frequently Asked Questions About 2026 Forgiveness

The new 10% debt relief program, effective April 2026, is a federal initiative designed to reduce the principal balance of qualifying student loans by up to 10%. This program aims to provide direct financial relief to borrowers, helping to alleviate their overall debt burden and potentially lower future payments.

Eligibility for the April 2026 debt relief primarily targets borrowers with federal Direct Loans. Specific criteria will likely include income thresholds and possibly repayment history. Borrowers with other federal loan types, like FFEL or Perkins, might need to consolidate their loans into Direct Loans to qualify.

Applications for the 10% debt relief program are expected to be available online through the official Federal Student Aid (FSA) website. You will typically need to provide personal identification, loan details, and income verification documents. Always ensure you are using official government channels to apply.

The 10% debt relief is generally expected to complement existing programs like PSLF. A reduction in your principal balance could mean a lower overall amount to be forgiven after completing your 120 qualifying payments. It should not negatively impact your PSLF progress but rather enhance your total relief.

Yes, it is highly probable that there will be income limits or thresholds for the 10% debt relief program. These limits are typically set to ensure that the relief is targeted towards borrowers who demonstrate a greater financial need. Specific income guidelines will be detailed on the Federal Student Aid website closer to April 2026.

Conclusion

The Federal Student Loan Forgiveness Program Updates for April 2026: Are You Eligible for the New 10% Debt Relief? represent a significant opportunity for millions of federal student loan borrowers to alleviate a portion of their educational debt. These ongoing efforts by the government underscore a commitment to addressing the student debt crisis and fostering greater financial stability for individuals and the broader economy. By staying informed, meticulously reviewing eligibility criteria, and proactively engaging with the application process, borrowers can effectively navigate these changes and maximize their benefits. The path to financial freedom from student loans may still be challenging, but with these new initiatives, it becomes more attainable for many.