Student Loan Forgiveness Programs 2026: Eligibility & Updates

Understanding the evolving landscape of federal student loan forgiveness programs in 2026 is vital for borrowers to determine their eligibility and navigate the application process for potential debt cancellation.

Navigating the complex world of student loan debt can be daunting, but as we look towards 2026, there are significant updates and considerations regarding student loan forgiveness 2026 programs that could profoundly impact your financial future. Whether you’re a recent graduate or have been managing loans for years, staying informed about federal policies and eligibility requirements is crucial for potentially erasing a portion, or even all, of your student debt.

understanding the current student loan landscape in 2026

The financial landscape for student loan borrowers continues to evolve, with 2026 bringing both continuity and modifications to existing federal programs. It’s essential for borrowers to differentiate between the various types of forgiveness and understand which programs remain active and how their criteria might have shifted. The goal is to provide clarity in a system often perceived as opaque.

Federal student loan forgiveness programs are not a one-size-fits-all solution; they are designed to address different financial situations and career paths. Staying updated on these programs ensures that you don’t miss out on opportunities for relief that you may rightfully qualify for. Many programs have specific requirements regarding loan type, repayment history, and employment.

key federal programs still active

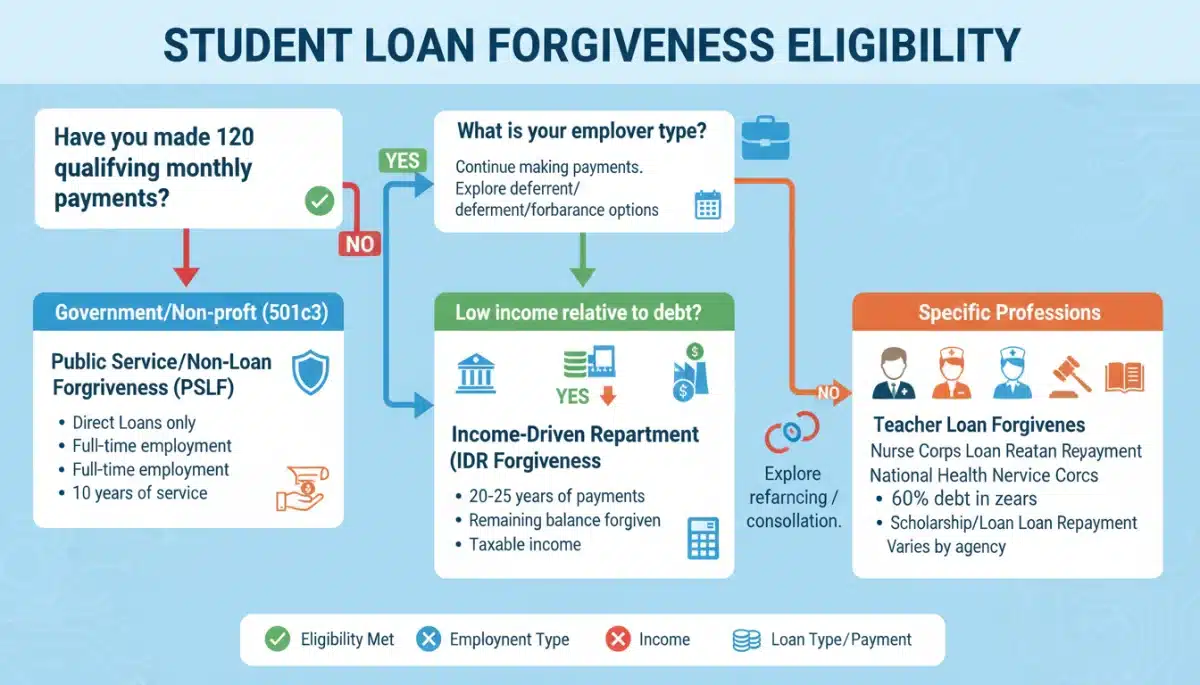

- Public Service Loan Forgiveness (PSLF): This program remains a cornerstone for individuals working in government or non-profit sectors.

- Teacher Loan Forgiveness (TLF): Designed for educators committed to serving in low-income schools, offering specific amounts of debt cancellation.

- Income-Driven Repayment (IDR) Plans: These plans offer forgiveness after a certain number of years of qualifying payments, adjusted to your income.

- Borrower Defense to Repayment: Continues to provide relief for borrowers whose schools engaged in misconduct.

Each of these programs has its own set of rules and application processes, which can be intricate. Understanding the core principles of each program is the first step towards determining potential eligibility. The federal government’s ongoing commitment to these initiatives reflects a broader effort to alleviate the burden of student debt across various sectors.

In summary, the 2026 student loan landscape emphasizes targeted relief through established federal programs. Borrowers are encouraged to research each program thoroughly and assess their individual circumstances against the outlined eligibility criteria. Proactive engagement with these options is key to securing potential financial relief.

eligibility criteria: what you need to know for 2026

Determining your eligibility for student loan forgiveness programs in 2026 requires a careful review of several factors, including your loan type, employment history, and income. These criteria are not static and can be subject to subtle changes, making it imperative to consult official sources for the most accurate and up-to-date information.

The federal government typically categorizes loans into different types, such as Direct Loans, FFEL Program loans, and Perkins Loans. Many forgiveness programs primarily target Direct Loans, though some provisions might allow consolidation of other loan types to become eligible. Employment is another significant factor, particularly for programs like PSLF and Teacher Loan Forgiveness, where specific types of service are required.

loan types and consolidation considerations

Not all student loans are created equal when it comes to forgiveness. Federal Direct Loans are generally the most eligible for a wide array of programs. If you have older FFEL or Perkins Loans, you might need to consolidate them into a Direct Consolidation Loan to qualify for certain benefits, including PSLF or IDR forgiveness.

It’s crucial to understand that consolidation can reset your payment count for IDR or PSLF, unless specific waivers or adjustments are in place. Always research the implications of consolidation thoroughly before proceeding, as it’s not always the best path for every borrower. The Department of Education provides comprehensive resources on this topic.

employment and income requirements

For programs like PSLF, working full-time for a qualifying employer (government organization or certain non-profits) is a fundamental requirement. You must make 120 qualifying payments while employed in such a role. Teacher Loan Forgiveness has specific requirements about teaching in low-income schools for a certain number of years.

Income-Driven Repayment plans, as their name suggests, base your monthly payments on your income and family size. After 20 or 25 years of qualifying payments (depending on the plan and whether you have graduate loans), any remaining balance is forgiven. These plans are particularly beneficial for borrowers with high debt relative to their income.

In essence, eligibility for 2026 forgiveness programs is multifaceted. Borrowers must align their loan types with program requirements, ensure their employment qualifies, and understand how their income impacts their repayment and potential forgiveness outcomes. A thorough self-assessment against these criteria is indispensable.

navigating the application process for federal forgiveness

Once you’ve determined your potential eligibility for a federal student loan forgiveness program in 2026, the next critical step is to navigate the application process. This involves understanding the necessary documentation, submission procedures, and the timelines involved. A meticulous approach here can significantly impact the success of your forgiveness claim.

The application process can vary depending on the specific program. While some programs, like PSLF, require annual employment certification, others may involve a single application upon meeting all criteria. It’s important to gather all required documents beforehand, such as employment verification, tax returns, and loan statements, to ensure a smooth submission.

essential documentation and forms

For PSLF, the primary form is the Public Service Loan Forgiveness (PSLF) & Temporary Expanded PSLF (TEPSLF) Certification & Application (ECF/Application). This form helps you track your qualifying employment and payments. For IDR plans, you’ll need to submit an Income-Driven Repayment Plan Request form annually to recertify your income and family size.

Teacher Loan Forgiveness requires a Teacher Loan Forgiveness Application upon completing your service requirement. Always ensure you are using the most current version of these forms, available on the Federal Student Aid website, to avoid any processing delays or rejections.

tips for a smooth application experience

- Keep meticulous records: Maintain copies of all submitted forms, employment verification, and payment histories.

- Communicate with your loan servicer: Regularly confirm that your loan servicer has accurate records of your qualifying payments and employment.

- Utilize online tools: Federal Student Aid offers online tools, such as the PSLF Help Tool, to assist in preparing and submitting your forms.

- Seek expert advice: If you encounter complex situations, consider consulting a financial advisor specializing in student loans.

The application process, while detailed, is manageable with proper preparation and attention to detail. Timely submission of accurate information is paramount. Any discrepancies or missing documentation can lead to delays or even denial of your forgiveness request, underscoring the need for careful execution.

In conclusion, a successful application for federal loan forgiveness in 2026 hinges on understanding the specific requirements of your chosen program, preparing all necessary documentation, and diligently following the submission guidelines. Proactive record-keeping and communication are your best allies in this process.

recent updates and changes affecting 2026 programs

The landscape of student loan forgiveness is dynamic, with federal policies and program rules subject to periodic adjustments. As we look towards 2026, it’s crucial for borrowers to be aware of any recent updates or legislative changes that could impact their eligibility or the benefits they receive. These changes often aim to streamline processes or expand access to relief.

Recent years have seen significant administrative actions and, in some cases, legislative proposals aimed at reforming student loan programs. While not all proposed changes come to fruition, understanding the direction of policy discussions can help borrowers anticipate future shifts. It’s wise to monitor official government announcements and reputable news sources for the latest information.

administrative adjustments to existing programs

The Department of Education has, in recent times, implemented administrative flexibilities and adjustments to existing programs. For example, some past payment counts for IDR and PSLF have been reviewed and updated to correct historical errors, potentially moving more borrowers closer to forgiveness. These adjustments often address issues such as forbearance steering or incorrect payment tracking.

Another area of focus has been on simplifying the application processes for certain programs. While the core requirements usually remain, efforts to make forms more user-friendly and provide clearer guidance can significantly benefit applicants. These administrative improvements aim to reduce barriers to access for eligible borrowers.

potential legislative changes on the horizon

While specific legislative changes for 2026 are not yet finalized, there are ongoing discussions in Congress regarding broader student loan reform. These discussions often include proposals for new forgiveness pathways, adjustments to interest rates, or changes to the structure of IDR plans. Such legislative actions, if passed, could introduce new opportunities or modify existing ones.

Borrowers should remain vigilant and not rely on speculation. Instead, focus on the programs currently in effect and confirmed policy changes. Any significant legislative overhaul would typically involve a period of implementation before taking full effect, providing some time for borrowers to adapt.

To summarize, the 2026 student loan forgiveness landscape is influenced by both ongoing administrative refinements and potential legislative developments. Staying informed about these updates through official channels is critical for all borrowers to effectively plan their repayment strategies and pursue available forgiveness opportunities.

understanding income-driven repayment (IDR) and forgiveness

Income-Driven Repayment (IDR) plans are a cornerstone of federal student loan relief, offering a pathway to forgiveness after a specified period of payments. For 2026, these plans continue to be a vital option for borrowers struggling with high debt-to-income ratios. Understanding how IDR works and its connection to forgiveness is essential for long-term financial planning.

IDR plans adjust your monthly student loan payment based on your discretionary income and family size. This ensures that your payments are affordable, even if your income is low. There are several IDR plans, each with slightly different formulas for calculating payments and different timelines for forgiveness, typically 20 or 25 years.

how IDR plans lead to forgiveness

Under an IDR plan, if you consistently make your reduced payments, any remaining loan balance is forgiven after the required number of years. This forgiveness is particularly beneficial for borrowers with substantial loan balances that they might never fully repay under standard plans. The key is to remain enrolled in an IDR plan and recertify your income annually.

The specific IDR plan you are on (e.g., REPAYE, PAYE, IBR, ICR) will determine the exact number of years required for forgiveness. It’s important to choose the plan that best suits your financial situation and long-term goals. The Federal Student Aid website provides tools to compare different IDR plans.

SAVE plan: a significant IDR update

The new Saving on a Valuable Education (SAVE) Plan, which continues into 2026, is a notable update to the IDR landscape. It offers potentially lower monthly payments than other IDR plans, especially for borrowers with lower incomes, and provides greater interest benefits. The SAVE plan replaces the REPAYE plan and is designed to significantly reduce the burden for many borrowers.

- Lower monthly payments: The SAVE plan calculates payments based on a smaller percentage of discretionary income compared to other IDR plans.

- Interest subsidy: Any unpaid interest that accrues after your monthly payment is covered by the government, preventing your loan balance from growing.

- Expanded income protection: A higher amount of income is protected from discretionary income calculations, further lowering payments for many.

The SAVE plan represents a significant shift in how IDR plans provide relief, aiming to make student loan repayment more manageable and forgiveness more attainable for a broader range of borrowers. Understanding its specific benefits and how it compares to other IDR options is crucial for making an informed decision.

In conclusion, Income-Driven Repayment plans, particularly the SAVE plan, offer a robust path to student loan forgiveness in 2026 by aligning payments with a borrower’s financial capacity. Consistent enrollment and annual recertification are vital steps towards achieving potential debt cancellation through these programs.

public service loan forgiveness (PSLF) in 2026

Public Service Loan Forgiveness (PSLF) remains a critical program for individuals dedicated to public service, offering a pathway to complete student loan forgiveness after 10 years of qualifying employment and payments. As we move into 2026, the core tenets of PSLF are expected to continue, providing stability for those in eligible professions.

PSLF is specifically designed for borrowers who work full-time for a U.S. federal, state, local, or tribal government agency or a qualifying non-profit organization. The program requires 120 qualifying monthly payments, which do not have to be consecutive, made under a qualifying repayment plan.

who qualifies for PSLF?

Eligibility for PSLF hinges on two main factors: your loans and your employment. Only Direct Loans qualify for PSLF. If you have FFEL or Perkins Loans, you’ll need to consolidate them into a Direct Consolidation Loan. However, prior payments made on those loans before consolidation generally do not count towards the 120 payments unless specific waivers or adjustments are in place.

Qualifying employment means working for a government organization (federal, state, local, or tribal) or a 501(c)(3) non-profit organization. Other non-profits may qualify if they provide specific public services. Full-time employment is generally defined as working at least 30 hours per week.

tracking your progress and applying

To ensure your payments and employment are being correctly tracked, it’s highly recommended to submit the PSLF & TEPSLF Certification & Application (ECF/Application) form annually, or whenever you change employers. This form allows your loan servicer to confirm your qualifying employment and update your payment count.

Once you have made 120 qualifying payments while working for a qualifying employer, you can submit the same form, indicating that you believe you have met the requirements for forgiveness. The Department of Education will then review your application and determine if you qualify for the remaining balance of your Direct Loans to be forgiven.

The PSLF program has undergone significant improvements and flexibilities in recent years, making it more accessible to eligible borrowers. These changes have addressed past administrative hurdles and expanded the types of payments that count towards the 120-payment requirement for some borrowers. Staying informed about these historical adjustments can be beneficial if you have a complex payment history.

In summary, PSLF in 2026 offers a powerful incentive for individuals pursuing careers in public service. Understanding the specific requirements for qualifying loans, employment, and payments, along with diligently tracking your progress, is paramount for successfully achieving student loan forgiveness through this invaluable program.

strategies for managing student loan debt in 2026

Beyond forgiveness programs, effectively managing your student loan debt in 2026 involves a combination of smart repayment strategies, financial planning, and staying proactive. Even if you don’t qualify for immediate forgiveness, there are numerous approaches to make your debt more manageable and work towards a debt-free future.

A personalized approach to debt management is key. What works for one borrower might not be ideal for another, depending on their loan types, interest rates, income, and financial goals. The goal is to minimize interest accrual, reduce monthly payments if needed, and ultimately accelerate your path to repayment.

exploring repayment options

If you’re not on an Income-Driven Repayment plan, consider if one is right for you. As discussed, IDR plans can significantly lower your monthly payments, making your debt more affordable. Another option is the standard repayment plan, which aims to pay off your loans in 10 years, often resulting in less interest paid over the life of the loan.

For borrowers with multiple federal loans, Direct Loan Consolidation can simplify your repayment by combining them into a single loan with one monthly payment. While it might extend your repayment period, it can make management easier. For some, refinancing private student loans (or even federal loans, though this forfeits federal benefits) with a private lender might offer lower interest rates, depending on your creditworthiness.

financial planning and budgeting

- Create a detailed budget: Understand your income and expenses to identify areas where you can save and allocate more funds towards your loans.

- Build an emergency fund: Having savings can prevent you from deferring payments or entering forbearance if unexpected financial hardship arises.

- Consider extra payments: If financially feasible, making extra payments can significantly reduce the principal balance and the total interest paid.

- Automate payments: Setting up automatic payments can ensure you never miss a due date, which can save you from late fees and negative impacts on your credit score.

Proactive financial planning is not just about paying off debt; it’s about building a stable financial future. Integrating student loan management into your broader financial strategy ensures that you are making informed decisions that align with your long-term goals. Regularly review your budget and repayment plan to make adjustments as your financial situation changes.

In conclusion, effective student loan debt management in 2026 involves a multifaceted strategy. From exploring suitable repayment plans and consolidation options to diligent budgeting and proactive financial planning, borrowers have a range of tools at their disposal to navigate their debt and work towards financial freedom.

| Key Program | Brief Description |

|---|---|

| PSLF | Forgiveness for public service workers after 120 qualifying payments. |

| IDR Plans (e.g., SAVE) | Payments based on income; forgiveness after 20-25 years. |

| Teacher Loan Forgiveness | Partial forgiveness for eligible teachers in low-income schools. |

| Borrower Defense | Relief for borrowers defrauded by their educational institution. |

frequently asked questions about student loan forgiveness 2026

Generally, federal Direct Loans are most eligible for forgiveness programs like PSLF and IDR. Older FFEL and Perkins Loans may require consolidation into a Direct Consolidation Loan to qualify for certain benefits. Private student loans typically do not qualify for federal forgiveness programs.

Your employment qualifies for PSLF if you work full-time for a U.S. federal, state, local, or tribal government organization, or a 501(c)(3) non-profit. Other non-profits may qualify if they provide specific public services. You should use the PSLF Help Tool to verify your employer’s eligibility.

The Saving on a Valuable Education (SAVE) Plan is an Income-Driven Repayment (IDR) plan that offers lower monthly payments and prevents interest from growing your loan balance. It can lead to forgiveness after 20 or 25 years of payments, making debt management more accessible for many borrowers.

While existing programs like PSLF and IDR (including the SAVE plan) are expected to continue, new legislative changes are always possible. Borrowers should monitor official announcements from the Department of Education or Congress for any significant new programs or modifications that might emerge.

First, thoroughly research the specific program requirements. Then, gather all necessary documentation, such as income verification and employment records. Contact your loan servicer to confirm your loan type and repayment history, and submit the appropriate application forms as directed by Federal Student Aid.

conclusion

As we navigate the complexities of student loan debt in 2026, the availability of federal forgiveness programs offers a vital lifeline for many Americans. Understanding the nuances of programs like PSLF, the various IDR plans including the SAVE plan, and other targeted relief initiatives is not merely an academic exercise; it’s a practical necessity for securing financial well-being. By staying informed about eligibility criteria, diligently following application processes, and adapting to ongoing policy updates, borrowers can effectively pursue the debt relief they may be entitled to, paving the way for a more stable and prosperous future.